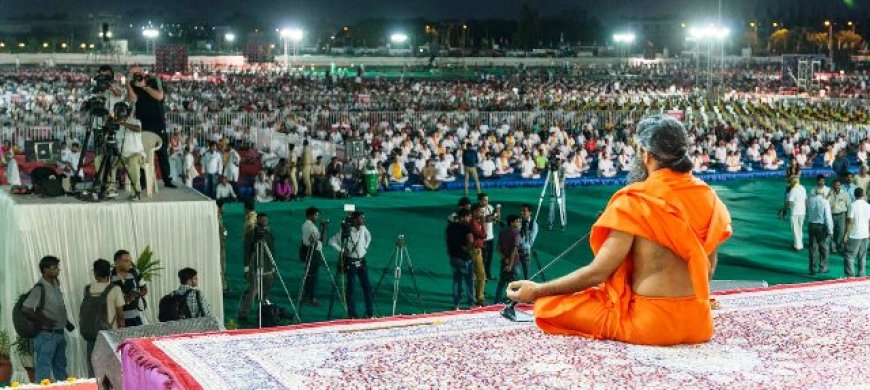

Ramdev Has To Pay Service Tax On Yoga Camps

n a setback to the Patanjali Yogpeeth Trust, the Supreme Court on Friday upheld an appellate tribunal's ruling that the organisation is liable to pay service tax for charging an entry fee for organising Yoga camps, both residential and non-residential.

In a setback to the Patanjali Yogpeeth Trust, the Supreme Court on Friday upheld an appellate tribunal's ruling that the organisation is liable to pay service tax for charging an entry fee for organising Yoga camps, both residential and non-residential.

A bench of Justices Abhay S Oka and Ujjal Bhuyan refused to interfere with the October 5, 2023 decision of the Allahabad bench of the Customs, Excise and Service Tax Appellate Tribunal (CESTAT).

The bench, while dismissing the Trust's appeal said, "The tribunal has rightly held that Yoga in camps for a fee is a service. We do not find any reason to interfere with the impugned order. The appeal is dismissed." In its order, the CESTAT had held that Yoga camps organised by Patanjali Yogpeeth Trust, which charges fees for participation, come under the category of "health and fitness service" and attract service tax.

"Though this amount was collected as a donation, it was fees for providing the said services and hence covered under the definition of consideration," it had noted, adding that the Commissioner of Customs and Central Excise, Meerut range has raised the service tax demand of approximately ₹ 4.5 crore for October, 2006 to March, 2011, with penalty and interest.

In its reply, the Trust had contended it was providing services which are for curing ailments. They are not taxable under "health and fitness service", it had said.

The appellate tribunal in its order said, "In our view the appellant (Patanjali Trust) was engaged in providing the services that were classifiable under the taxable category of services provided by health club and fitness centre, as defined under Section 65 (52) of the Finance Act, to any person.

The appellate tribunal said the Trust collected the entry fee disguising it as donation. "They issued entry tickets of various denominations. The holder of the ticket was granted different privileges depending on the denomination of the ticket. In return the appellant provided the person entry to the camp where Swami Baba Ramdev would give instructions in respect of Yoga and Meditation," it had said.

What's Your Reaction?